The projected Florida auto insurance refunds for the 2025 and 2026 fiscal and regulatory cycle undoubtedly represent one of the most momentous financial, legal, and consumer protection milestones in the contemporary history of the Southeastern United States insurance market. With the official confirmation that direct-sales corporate titans, led by Progressive Insurance and followed in analytical projections by similar-caliber corporations like Geico, State Farm, and Allstate, will collectively return nearly $1 billion to Floridian drivers, the public and political narrative has tended to celebrate this event as an absolute victory for the common citizen’s economy. However, an exhaustive, structural, and dispassionate financial analysis of this phenomenon reveals an underlying reality that is much more complex and troubling for the long-term financial health of policyholders: massive refunds are not corporate gifts, acts of goodwill, or efficiency dividends, but the mandatory and delayed legal correction of a systematic overpricing in premiums charged during 2023 and 2024.

This research report breaks down with academic meticulousness, actuarial rigor, and analytical expertise the economic forces, the volatile legislative statutes, and the recent tort reforms that have triggered this massive return of capital. More importantly, this document critically re-evaluates the very concept of the “refund.” By contrasting this reactive model, characteristic of direct and captive insurers, with the proactive and technologically advanced value proposition of leading independent agencies like Univista Insurance, a fundamental thesis is exposed: paying the right price from day one is mathematically superior to financing a corporation’s excess profits. By leveraging cutting-edge comparative technology, simultaneous quoting platforms, and a fiduciary approach focused on the local market, Univista Insurance neutralizes the need for future refunds by ensuring that the consumer pays exclusively the mathematically fair price for their coverage, thus protecting the citizen’s liquidity and opportunity cost.

The Structural Transformation and Historical Crisis of the Florida Auto Insurance Market (2015-2026)

To fully understand the magnitude and inevitability of the statutory refund phenomenon dominating the 2026 headlines, it is imperative to first examine the profound systemic crisis from which the Florida market emerges. For more than a decade, the “Sunshine State” operated under a highly volatile, dysfunctional, and exceptionally litigious regulatory and legal environment. This ecosystem was characterized by chronic abuses in the judicial system, the proliferation of frivolous “bad faith” lawsuits, the exploitation of assignment of benefits (AOB), and the application of attorney fee multipliers that artificially and exponentially inflated the cost of resolving nearly every claim.

The Asymmetrical Cost of Litigation and the Flight of Insurance Capital

Historically, the OIR, along with independent analysts and legislative watchdog groups, documented an astonishing asymmetry: although the state of Florida accounted for barely a single-digit percentage (approximately 9%) of the total volume of insurance claims nationwide, it simultaneously housed an overwhelming proportion (close to 79% in certain property and casualty lines) of all insurance litigation in the country.

Exhaustive government reports pointed out that, over a critical ten-year period, a staggering 71% of the $51 billion paid by insurers operating in Florida did not go toward the legitimate repair of vehicles, compensating accident victims, or rebuilding property, but was diverted directly to paying plaintiff attorneys’ fees and public adjusters. In short, legal intermediaries received substantially more money from claim settlements than the actual policyholders who had suffered the losses.

This structural, deeply rooted inefficiency forced auto insurance companies to recalibrate their risk models toward the most conservative extreme. To maintain the technical solvency required by the state and avoid bankruptcy in the face of relentless legal assaults, insurers increased their premiums drastically and relentlessly. The average Florida driver was forced to subsidize a broken legal system. This escalation reached its peak at the beginning of the current decade; as recently as 2023, major auto insurance groups experienced approved average rate increases of 31.7%, strangling the budgets of countless families and small businesses.

The Legislative Turning Point: The 2022 and 2023 Reforms (HB 837 and SB 2A)

The imminent collapse of the market demanded unprecedented state intervention. The definitive turning point arrived with the enactment of comprehensive and far-reaching tort reform bills, highlighting the HB 837 legislation signed in March 2023 by Governor Ron DeSantis, complemented by the prior SB 2A legislation. These laws dismantled the architecture of legal abuse in Florida and permanently altered the trajectory of the insurance market.

The legislation implemented strict controls and fundamental recalibrations on the civil system, establishing the following structural regulations:

- Reduction of the Statute of Limitations: The timeframe to file general negligence lawsuits was significantly shortened, forcing a faster resolution of claims and limiting insurers’ long-tail exposure.

- Implementation of a Modified Comparative Negligence Standard: This was a seismic shift. Under this new standard, a plaintiff determined by a court or jury to be more than 50% at fault for their own injuries or damages is barred from recovering any financial compensation. This immediately eliminated thousands of speculative lawsuits where the primarily at-fault party sought a financial settlement.

- Severe Restriction on Bad Faith Lawsuits: The law explicitly required policyholders and third-party claimants to act in good faith in their interactions. Furthermore, it provided insurers with a legal “safe harbor” if they pay the policy limits within a specific timeframe, eliminating the extortionate tactic of setting insurers up for failure in claim handling only to sue them for extracontractual amounts.

- New Standards of Proof for Medical Expenses: The legislation prevented “phantom” or artificially inflated medical bills from being presented as actual damages in trials, requiring juries to consider the amounts actually paid and accepted by healthcare providers, not the initial inflated billed charges.

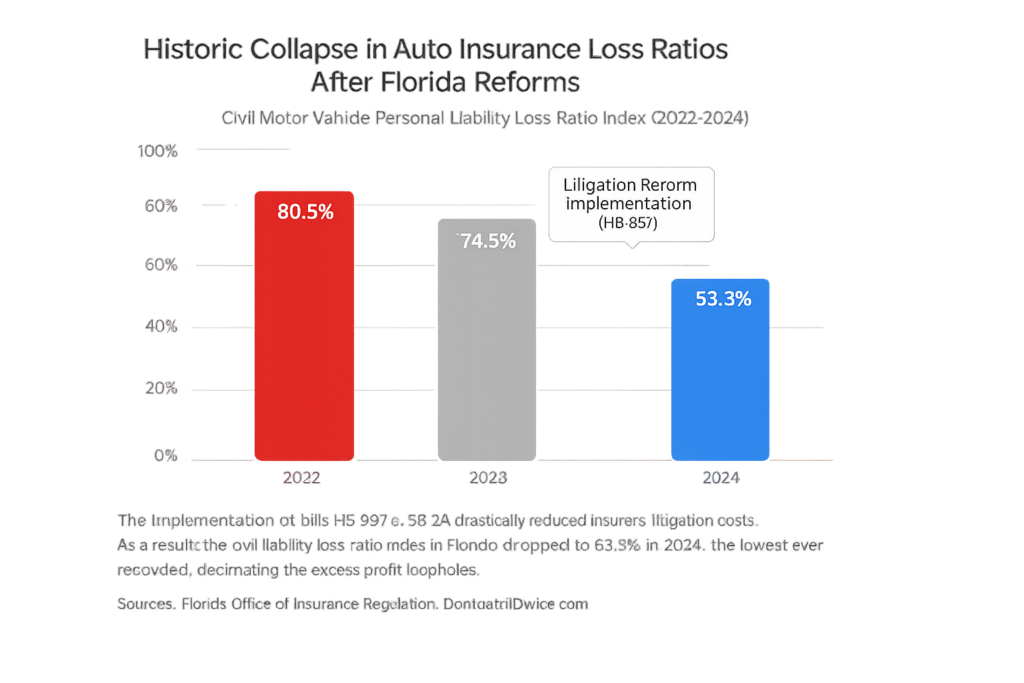

The impact of these structural reforms was almost immediate on insurers’ ledgers, profit and loss statements, and reserves. As the constant threat of prolonged litigation, fee multipliers, and coerced settlements disappeared overnight, loss ratios and loss adjustment expenses (LAE) plummeted to levels not seen in decades.

As confirmed by official records from the OIR and Commissioner Michael Yaworsky, the personal auto liability loss ratio dropped drastically from 80.5% in 2022 to 74.5% in 2023, and finally plummeted to an astonishing 53.3% in 2024. This indicator positioned Florida, which for years was the most problematic state, with the lowest loss ratio in the entire United States during that period.

This seismic improvement in profitability far exceeded even the most optimistic internal actuarial projections of the insurers themselves. Direct-sales companies had set their regulatory rates for 2023 and 2024 anticipating the continuation of the burdensome and extortionate litigation environment of the past. As the massive savings from the legislative reforms materialized, but the historically high premiums continued to be collected, insurers began to post multi-million dollar net profits quarterly—profits that would eventually exceed the statutory limits permitted by Florida law.

Anatomy of the Progressive Refunds, the Projection Toward Geico, and the Direct Ecosystem

In late 2025 and early 2026, the inescapable mathematical reality of low claims colliding head-on with pre-existing high rates converged into a massive and unprecedented regulatory event. Progressive Insurance, the largest private passenger auto insurance carrier by market share in the state of Florida, formally acknowledged through financial disclosures to the U.S. Securities and Exchange Commission (SEC) and in communications with the OIR that its operating profits would exceed the triennial legal limits.

Quantitative Breakdown of Progressive’s “Mega Refund”

In a highly publicized press conference led by Governor Ron DeSantis, flanked by Insurance Commissioner Michael Yaworsky and Chief Financial Officer Jimmy Patronis, it was confirmed to the media and citizens that Progressive would return a historic volume of approximately $950 million (nearly $1 billion) to Florida resident drivers.

The operational, financial, and logistical parameters of this monumental refund were established under strict guidelines:

- Volume of Affected Consumers: An estimated 2.7 million personal auto insurance policyholders in Florida qualify under the initial criteria for premium returns.

- Average Refund Amount: The average refund or credit has been actuarially calculated at around $300 per vehicle policy. However, company spokespeople like Jeff Sibel have clarified that the exact and final credit amount for each policyholder will vary proportionally based on the total earned premium of each policy during the 2025 calendar year and will depend on the audit of year-end financial results.

- Distribution Mechanism and Accounting Treatment: The funds will be treated for accounting purposes as a policyholder dividend applicable to the year in which it was incurred. For the vast majority of Progressive customers, this will be reflected as a credit automatically applied to their renewal bill in early 2026. In scenarios where a driver has a zero balance with the insurer, or if the credit is larger than their next scheduled payment, statutes and regulations require a payment to be issued to the customer through the same original method used to pay premiums (e.g., direct deposit or a physical check sent via postal mail).

The Domino Effect: Geico and the Rest of the Market Oligopoly

The structural impact of this excess profit regulation is by no means limited to Progressive. Governor DeSantis, recognizing the identical dynamics operating in the profit margins of other direct mega-insurers, has been emphatic in publicly declaring: “I don’t think there’s any reason to think these other companies are any different than Progressive. I think you’re going to see rebates. I think you’re going to see maybe checks, however they decide to do it.”

In response to Progressive’s proactive initiative to “come to the table first,” authorities from the Florida Office of Insurance Regulation immediately initiated aggressive rounds of negotiations with the other four top companies that, alongside Progressive, control 78% of the auto insurance market in the state. This quintet of industry leadership includes corporate giants such as Geico, State Farm, Allstate, and USAA.

Coordinated regulatory pressure and public scrutiny set a clear analytical expectation: throughout 2026, the market will witness multiple cascading announcements from companies like Geico, finding themselves legally obligated to issue their own multi-million dollar statutory refunds, or alternatively, to make even more drastic and accelerated base rate reductions to rapidly purge the excess capital accumulated on their balance sheets during the 2024 and 2025 market correction. In fact, preliminary OIR data already indicates that the top 5 insurance groups averaged a requested rate reduction of 6.5% for 2025, with filed reductions of up to 11.5% in certain risk brackets.

| Insurance Group (Top 5 FL Market) | Combined Market Share | Average Rate Adjustment (2025) | Excess Profit Refund Status (2026 Projection) |

| Progressive Insurance | ~15-20% | Requested Reduction | Confirmed: ~$950 Million in credits/checks. |

| Geico | ~15-20% | Requested Reduction | In OIR Negotiation: High probability of imminent statutory refunds. |

| State Farm | ~15-20% | Requested Reduction | Under Actuarial Review: Subject to evaluation of the 2023-2025 period. |

| Allstate | ~10-15% | Requested Reduction | Under Actuarial Review: Subject to evaluation of the 2023-2025 period. |

| USAA | ~5-10% | Requested Reduction | Under Actuarial Review: Subject to evaluation of the 2023-2025 period. |

| Note: Data derived from statements by the OIR and the Governor’s office. The Top 5 controls 78% of the total Florida market. | |||

Legal and Regulatory Deconstruction: Florida Statute 627.066 and the Mechanics of Excess Profits

For a researcher, a stock market financial analyst, or an educated consumer to truly understand why for-profit, publicly traded corporations are voluntarily (and simultaneously mandatorily) returning nearly a billion dollars, it is essential to deconstruct the legal text acting as the Sword of Damocles over the industry: Florida Statute 627.066, formally titled “Excessive profits for motor vehicle insurance prohibited.”

Originally passed in the late 1970s during an administration and legislature with a different political composition, this legislation has endured as an exceptionally powerful consumer protection mechanism of last resort. Its intrinsic legislative purpose is to prevent insurance companies from reaping monopoly rents, unearned windfalls, or maintaining the accumulation of capital derived from rates that have become chronically misaligned with the actual risk and claim volume of the population.

The Mathematical Formula for Excessive Profit

The statute does not operate on the basis of vague estimates; it imposes a strict, codified, and auditable mathematical limit on the profitability of business lines defined as “private passenger automobile business,” explicitly excluding commercial auto insurance.

According to section (3)(a) of the law, an “excessive profit” is statutorily considered to have been obtained and consolidated if the following financial condition occurs:

“Excessive profit has been realized if there has been an underwriting gain for the 3 most recent calendar-accident years combined which is greater than the anticipated underwriting profit plus 5 percent of earned premiums for those calendar-accident years.”

To transparently calculate the underwriting gain, the State of Florida instructs an accounting subtraction formula. It starts with the calendar-year earned premium and subtracts the total sum of three main components:

- Losses: Accident-year incurred losses plus corresponding loss adjustment expenses, developed to an ultimate basis as of March 31 of the following year.

- Operating Costs: General administrative expenses and selling expenses incurred specifically within the state of Florida or logically allocated to the state’s operations during the calendar year.

- Prior Returns: Policyholder dividends applicable to that calendar year.

The Rolling Triennial Trigger (The 2023-2025 Block)

The most critical, ingenious, and simultaneously complex aspect of this statute is that it does not evaluate an insurer’s financial performance year-by-year in isolation. To smooth out the inherent volatility of the insurance business (such as seasonal accident spikes or minor weather impacts), the State requires the evaluation to be conducted in rolling blocks of three consecutive years.

It is precisely this time window that caught the pricing models of the major direct insurers. Progressive openly admitted in its financial filing with the SEC that the immense combined profitability of the 2023, 2024, and 2025 block would inevitably surpass the legal ceiling of “anticipated underwriting profit plus 5%.”

Although corporations began to gradually adjust and reduce projected base rates for 2025, these late reductions were not swift, substantial, or deep enough to mathematically counteract the massive profit margins accumulated throughout 2023 and 2024. It was during those months, immediately following the implementation of the 2023 tort reforms, when litigation and claim costs went into a vertical nosedive, yet Florida consumers diligently continued paying inflated premiums dictated by the obsolete actuarial models of the past.

The law is draconian and unyielding in its remedy. It explicitly dictates in subsection (9): “Any excess profit of an insurance company offering motor vehicle insurance shall be returned to policyholders in the form of a cash refund or a credit towards the future purchase of insurance.”

The Hidden and Harmful Truth of Refunds: Opportunity Cost, the Eligibility Trap, and Consumer Detriment

At first glance, and through the lens of public relations campaigns, news headlines broadly proclaiming “$1 billion in auto insurance refunds for Floridians” have been processed in mass media discourse as an economic windfall from the sky and a testament to the overwhelming success of government policy. From the state’s political, legislative, and macroeconomic viewpoint, it certainly is; it demonstrates that judicial reforms worked and that the OIR has the capacity and legal “teeth” to enforce the law and compel multinational corporations to return capital to citizens.

However, from the microeconomic perspective, from the financial reality of the everyday driver’s monthly budget and personal finances, a statutory refund under the mandate of F.S. 627.066 is no reason for unconditional celebration. On the contrary, it is empirical forensic evidence of profound inefficiency in the direct market and the symptom of sustained economic detriment against the policyholder.

The “Zero-Interest Loan” Theory and the Destruction of Opportunity Cost

When a Floridian driver receives a check or bill credit for an average of $300 in the mail in early 2026, the undeniable mathematical and financial implication is that, during the immediately preceding 36 months, that person, that family, overpaid by at least $300 for coverage that had a fundamentally lower risk cost.

In strict financial terms, millions of Florida citizens unknowingly, involuntarily, and without their explicit contractual consent, extended a zero-percent interest loan totaling nearly $1 billion to some of the wealthiest, most liquid, and profitable financial corporations and capital institutions on the planet.

Consider the underlying macroeconomic environment during that period (2023-2025): it was an era characterized by stubborn inflation and the highest Federal Reserve interest rates in nearly two decades. While the receiving corporations reported stellar quarterly net incomes in the billions, inflating their stock market value and generating prodigious returns by aggressively reinvesting that massive premium surplus into capital and bond markets, the average Floridian consumer suffered the direct impact of the cost of living.

The everyday citizen lacked access to that $300 of liquid capital that rightfully belonged to them. It could have been invested in index funds, used to pay down high-interest credit card debt, or simply allocated to family sustenance. The legal statute rigorously compels the corporation to return the overcharged principal, but Florida law does not require the insurer to compensate or reimburse the customer for the monumental opportunity cost of the capital lost over those three long years. The true financial winner during that period of arbitrage was not the consumer, it was the insurer’s shareholder.

The Structural Injustice: The Eligibility Trap and the Loss of the Refund

The most controversial, financially punitive, and detrimental aspect of the current structure of statutory refunds lies in the arbitrary eligibility criteria based on a “cutoff date” imposed by the corporation. According to official statements, authorized Progressive spokespeople, and technical guidelines published by the OIR, the insurer will only issue credits or refund checks to those drivers who actively maintain an in-force policy on or after the arbitrary deadline of December 31, 2025.

This rigid rule creates a profoundly unfair externality that has generated confusion, anger, and severe documented complaints among the state’s consumers. Consider the following analytical scenario, which illustrates the systemic failure of this approach:

- A responsible and diligent Florida driver was insured under the direct model throughout 2023 and 2024. They patiently endured and paid month-by-month the highest premiums in the state’s history, contributing directly, substantially, and mathematically to the accumulation of that very same “excess profit” that the company recorded on its books during that biennial block.

- Frustrated, drowning in continuous high costs, and exercising their fundamental right as an actor in a free-enterprise market, this proactive consumer researches, gets quotes, and decides to seek a better rate more aligned with their low-risk profile. They finally switch insurance companies and cancel their original policy in, say, September 2025.

- The bleak outcome: Despite having funded the vast majority of the corporate excess profit with the sweat of their brow during twenty-four critical months, this specific consumer will not receive a single cent in refund or compensation. The wealth they generated will be redistributed or absorbed, but it will not return to their pocket, simply because their contract was not active at the exact minute the clock struck midnight on December 31, 2025.

This requirement to maintain an active captive policy ironically punishes the proactive, intelligent, and economically rational consumer who sought better options in the free market, while it financially rewards inertia, apathy, and brand dependency. This phenomenon starkly reveals an inherent structural flaw in the model of direct dependency on a single massive provider that unilaterally dictates its own centralized rates.

Univista Insurance’s Strategic Paradigm: The Superiority of Upfront Precision vs. Reactive Refunds

Faced with the overwhelming historical and mathematical evidence that direct insurer models almost inevitably lead to vicious cycles of prolonged periods of overcharging, followed eventually by state interventions and reactive corrections (refunds with expiration dates), the urgent need for a radically different approach emerges. The Florida consumer demands a system that is more sophisticated, transparent, customer-centric, and above all, economically efficient.

It is precisely at this critical intersection where the independent agency brokerage model, perfected to institutional levels by corporations like Univista Insurance, demonstrates fundamental tactical superiority and indisputably positions itself as the methodological gold standard for acquiring the best auto insurance in Florida in the post-2026 era.

The Actuarial Philosophy of Upfront Precision vs. The Corporate Loan

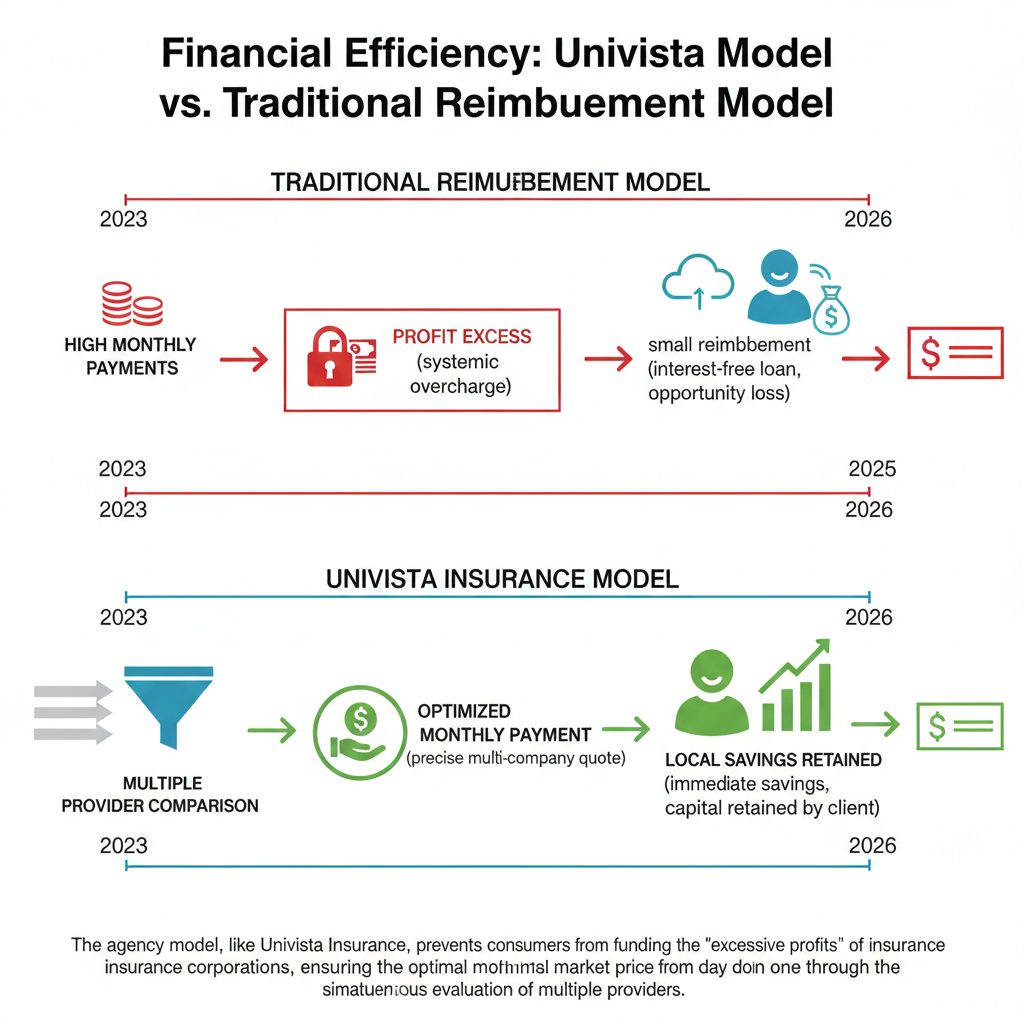

Univista Insurance’s core value proposition and economic moat are not based on fleeting marketing tactics, but on a simple yet devastatingly powerful principle of economic efficiency: It is infinitely and mathematically better to pay the exact, rigorous, and fair price from the first day of coverage than to passively finance a corporation by overpaying, hoping to recover a fraction of that money years later through a mandatory and conditional government refund.

Unlike the direct model, Univista Insurance is not a captive insurance company whose primary function and fiduciary duty is to maximize the quarterly profit margin of a single internal corporate product or please a board of directors focused on a single balance sheet. In essence, Univista functions operationally as a fiduciary advisor and an advocate broker for the client. When a Florida citizen, whether in Miami, Hialeah, Pembroke Pines, or anywhere in the state, requests auto insurance quotes at Univista’s facilities, the agency’s technology does not issue a monolithic, static, or “take it or leave it” style price.

Instead, Univista’s advanced technological ecosystem simultaneously interrogates, through high-speed APIs and direct connections, the quoting databases of dozens of the most competitive, solvent, and financially “A”-rated carriers operating in the state of Florida.

By relentlessly forcing these multiple insurers to compete in real-time, side-by-side, for the privilege of underwriting the client’s policy risk on a single unified screen, Univista inherently eliminates the monopolistic pricing inefficiencies that plague the direct market. If a particular massive company (as might have been the case with Progressive, Geico, or State Farm in the uncertain 2023 period) is suffering from actuarial paranoia, overestimating risk, and charging premiums that would eventually generate the infamous “excess profit,” Univista’s quoting algorithm will simply discard it to the side. Immediately, the platform will highlight, favor, and recommend a competitor (whether highly efficient regional carriers or better-calibrated national giants) that has adjusted its rates more fairly, precisely, and actuarially soundly for the exact moment and risk profile of the present.

This miniature free-market dynamic proactively protects the client’s liquid capital month after month. With Univista Insurance on their side, the $300 or more that a company like Progressive would promise to bureaucratically return in 2026 never leaves the consumer’s pocket in the first place. That precious capital remains safe in the Floridian family’s bank account, available for their own immediate needs and generating returns for their own economic benefit, instead of languishing in an insurance corporation’s treasury for three years.

Infrastructure, Community Leadership, and Expansion: Univista’s Corporate Backing

For an independent brokerage model to work at the massive scale required to influence the market of a state the size of Florida, it requires formidable corporate infrastructure, heavyweight industry alliances, and leadership with a visceral understanding of local realities.

Founded over 15 years ago under the visionary leadership and tenacity of CEO Ivan Herrera, Univista Insurance has rapidly transcended the modest label of a neighborhood insurance agency to consolidate itself as a true financial and insurance distribution powerhouse at the regional level and with a growing national presence. The corporation understands the unique economic pressures and demographic dynamics of the communities it serves, maintaining a particular, deep, and culturally rooted focus on empowering and protecting the Hispanic ecosystem in the United States.

The overwhelming success, institutional reliability, and strength of Univista’s franchise and direct office model are solidly backed by verifiable financial metrics, third-party audits, and irrefutable journalistic recognition in the business sphere:

- Dominance in the South Florida Business Journal (SFBJ) Rankings: Year after year, Univista Insurance has been consistently evaluated and ranked as one of the largest and most financially healthy private corporations in South Florida. It rapidly climbed the rigorous ranks of the publication, placing 54th on the elite Top 100 Private Companies list. Even more impressive in its specific sector, it has firmly consolidated itself within the illustrious Top 4 insurance agencies operating across the entire southern region.

- Sustained Growth, Revenue, and Distribution Infrastructure: Defying industry consolidation trends, the company has consistently reported over $90 million in combined gross revenue in recent periods, sustaining its meteoric rise with over $480 million in brokered premium volume in the vital South Florida corridor alone. This massive logistical and commercial operation relies on an extensive network of over 151 strategic physical locations, including imposing corporate centers, state-of-the-art call centers, and more than 141 highly successful franchises. Furthermore, demonstrating the national scalability of its model, the company has aggressively expanded its operational footprint far beyond Florida’s borders, opening operations in key demographic markets such as Texas, California, Georgia, North Carolina, and Arizona.

- National Recognition and Institutional Capital Injection: Beyond state lines, Univista’s corporate excellence was validated by its inclusion in the prestigious and coveted Inc. 5000 list, which catalogs the fastest-growing private companies across the United States. Simultaneously, it was ranked on the elite national list of large property and casualty insurance agencies by the publication Insurance Journal. The ultimate testament to the long-term viability and solidity of its Hispanic-focused distribution model occurred recently when the private equity arm GRAM Americas Buyout Fund, an entity with vast resources and global affiliations such as Grupo Romero and former Carlyle executives, executed a majority investment in UniVista Insurance, injecting capital, corporate strategic expertise, and signaling solid Wall Street institutional backing for its business model.

| Leadership and Expansion Metric | Univista Insurance Institutional Achievement | Impact on the Florida Consumer |

| Premium Volume (South FL) | Over $480 Million in brokered volume. | Massive negotiating power with insurers to secure low and preferential rates. |

| SFBJ Ranking (Private Companies) | Ranked #54 out of the 100 largest corporations. | Guaranteed financial stability; a solid corporation backing the policies. |

| Sectoral Ranking (SFBJ) | Top 4 Insurance Agencies in South Florida. | Proven expertise compared to direct competitors or smaller-scale brokers. |

| Physical Presence and Infrastructure | 151+ locations, including 141+ franchises and 1,200+ agents. | Unrivaled accessibility. In-person community support in Miami, Hialeah, and statewide. |

| Institutional Backing and Capital | Acquisition and investment by GRAM Americas Buyout Fund. | Capacity for continuous investment in better technology, customer service, and national expansion. |

The unique combination of possessing enormous corporate scale, statewide negotiating power with carriers, and hyper-localized attention through thousands of agents rooted in communities like Miami, Hialeah, and Pembroke Pines, means that Univista Insurance operates at the perfect intersection of power and empathy. It can negotiate and interact with multinational mega-insurers on absolute equal terms, demanding the best rates, while jealously maintaining the cultural sensitivity, language, and human community connection necessary to educate, guide, and protect the end customer with unwavering honesty and deep local expertise.

Technological Innovation at the Service of the Insured: Zero Friction

In the hyper-connected, instant-gratification ecosystem of the 2026 insurance market, convenience, information transparency, and transactional agility are almost as crucial as the premium price itself. Anticipating this evolution in consumer behavior, Univista Insurance has drastically mitigated the classic friction associated with the quoting, purchasing, and policy management process through multi-million dollar investments in in-house software development, resulting in a robust, intuitive, and industry-leading technological suite.

Unlike the often demoralizing experience of trying to navigate a massive corporation’s automated phone systems and overwhelmed customer service during peak hurricane season or chaotic refund issuance periods (times when thousands of customers report endless wait times, disconnections, and widespread frustration with direct lines), Univista offers a truly seamless, user-centric omnichannel ecosystem:

- Univista Insurance Mobile App (iOS and Android): The pinnacle of this digital strategy is its native mobile application. Highly rated in major app stores, it allows users to manage the entire lifecycle of their policies from the palm of their hand. It allows them to view coverages, instantly access and download digital ID cards critical for traffic stops or accidents, make secure payments, and, most importantly from a free-market perspective, compare new rates in real-time. In its latest major iteration (version 4.1.0 and higher), the platform integrated full and native bilingual support (switching effortlessly between Spanish and English). Additionally, the app made a qualitative leap by introducing 24/7 virtual assistance through “Mayra,” a sophisticated avatar and Artificial Intelligence engine meticulously trained on company manuals to resolve complex questions about coverage needs and state regulations instantly, regardless of the time of day.

- Smart and No-Obligation Digital Quoting Process: Through the corporate web platform and the app’s architecture, the process of obtaining multiline quotes is fluid and 100% digital. Users input a basic profile, minimizing paperwork. In a matter of milliseconds, the platform’s algorithmic engine evaluates dozens of underwriting variables and transparently returns a menu of competitive options. According to historical and internal company reports, corroborated by a staggering 98% satisfaction rate, this hyper-efficient comparison model manages to generate options that allow drivers to save up to an astonishing 40% in costs compared to inaction and blind passive renewal with prior carriers dictating local monopolies.

Portfolio Diversification: The Financial Power and Synergy of “Bundling”

While auto insurance refunds currently capture media spotlights and monopolize the short-term financial conversation, the truly sophisticated consumer in Florida understands that motor vehicle insurance is only one facet of a comprehensive family risk management portfolio. Relying on a monolithic direct provider for auto, and then trying to find another isolated provider for home or health, creates a costly, inefficient administrative puzzle plagued with coverage gaps.

Univista Insurance’s service architecture shines exceptionally as a one-stop-shop solution for holistic family and business risk management. The platform and expert agent network are not limited to four wheels; they facilitate the comprehensive consolidation of critical protections. In addition to insuring every conceivable type of vehicle (family cars, truck fleets, motorcycles, boats, as well as facilitating complex and high-risk state filings like the SR-22 and FR-44 certifications required by the DMV), Univista is a dominant player and an undisputed leader in providing the following lines of financial defense:

- Home and Property Insurance in Hurricane Zones: Providing everything from standard HO3 policies to specialized HO6 policies for condos and flood insurance (FEMA or private), navigating the complex Florida property market battered by natural disasters.

- Commercial and General Liability Insurance: Protecting the backbone of the Floridian economy by structuring complex policies for small and medium-sized businesses, contractors, and workers’ compensation, shielding the assets of Latino and general entrepreneurs against civil liability lawsuits.

- Advanced Life Insurance and Retirement Planning: Breaking traditional taboos, Univista advisors actively educate on and market permanent and term policies, highlighting crucial industry modernizations such as life insurance with living benefits in Florida. These innovative policies allow, through accelerated riders, access to substantial tax-free funds while the insured is still alive to face catastrophic expenses originating from chronic, terminal illnesses, or prolonged care, acting as a dual shield against medical bankruptcy.

- Health Insurance and Government Navigation: Acting as expert guides through the complex bureaucracy of government Health Insurance Marketplaces. Certified and award-winning agents (like CEO Ivan Herrera, recognized by the Centers for Medicare & Medicaid Services (CMS) in the prestigious “Marketplace Circle of Champions”) assist families in maximizing subsidies under the Affordable Care Act (Obamacare) and selecting the most efficient and comprehensive Medicare Advantage plans for seniors.

The financial synergy of this diversification is mathematical. Consolidating or bundling multiple disparate policies under the unified guidance of the same expert independent agency, like Univista, is not simply convenient; it is one of the most potent, proven, and consistent actuarial strategies to unlock substantial, deep, and permanent multiline discounts through partner carriers, maximizing the value of every dollar spent on asset protection.

The Definitive FAQ Guide on the 2026 Florida Market

With the massive overload of often contradictory information circulating in morning news, social media platforms, and political discourse surrounding recent government actions and capital returns, it is imperative to clear the “white noise.” Below, we clarify in a structured, objective, and definitive manner the technical, legal, and financial aspects most queried by the population regarding the complex auto insurance environment in Florida.

What exactly, in simple terms, is the Florida Excessive Profits Statute (627.066)?

Revised Florida Statute 627.066 is a fundamental consumer financial protection law enacted decades ago that explicitly and mathematically prohibits private passenger auto insurers from retaining and hiding unreasonable, usurious, or unjustifiably high profit margins at the expense of citizens. The law’s mechanics dictate that if an insurer’s actual underwriting gain exceeds its projected anticipated gain (plus a 5% operating cushion margin) on a sustained basis for three consecutive calendar-accident years, the corporation loses the right to keep that money. The law imposes a non-negotiable mandate on the company to return 100% of that excess equity capital directly to the pockets of affected policyholders, operating by issuing credits on future bills or sending cash refund checks.

Why are corporations like Progressive and, according to forecasts, other giant insurers announcing and issuing these massive refunds right now, in 2025 and 2026?

The monumental corporate refund of nearly $1 billion in Florida is not an isolated economic miracle or an act of insurer altruism. It was mandatorily triggered because the historic civil litigation and procedural abuse reform of Florida, codified and passed in 2023 (HB 837 and SB 2A), worked exceptionally well. These laws drastically, immediately, and statewide reduced astronomical legal defense costs, inflated attorney fees, and proliferating speculative “bad faith” lawsuits. As a direct consequence, large direct insurers experienced unexpectedly massive profitability because they had continued charging very high premiums in 2023 and 2024 (erroneously anticipating the continued paralyzing high litigation costs of the previous regime), but in the post-reform reality, they ended up paying immensely smaller sums and processing less capital volume in claim resolutions and trials. By trapping more money in premiums than they could legally retain against their low losses, the guillotine of the Excessive Profits Statute was activated.

Who exactly qualifies to be a recipient and receive the Progressive insurance refund credit scheduled for early 2026?

To qualify to receive Progressive’s financial refunds strictly related to the excess profit block of the 2023-2025 operating cycle, the primary and most restrictive requirement dictated unilaterally by the company’s corporate policies is to own and maintain an active, in-force policy in the state of Florida on or after the deadline of December 31, 2025. Highly controversially and unfortunately, those customers who stoically paid record premiums throughout 2023 or 2024 (de facto funding much of those excess profits), but who moved out of state, sold their vehicle, or simply decided to exercise the free market and switch insurance companies before December 31, 2025, are systematically disqualified and are not eligible to receive any portion of the multi-million dollar return.

How can the architecture of an independent insurance agency like Univista Insurance protect me financially, in the long term, from overpaying for my coverages?

Unlike the structure and operation of a captive agent (direct employees who exclusively represent a single corporate brand and who, by mandate, can only offer and sell you the price dictated by their parent company, regardless of how high or disconnected from reality it is), a truly independent agency like Univista Insurance operates without monopolistic conflicts of interest. When you get a quote at Univista, the agency enters your profile and detailed risk metrics into a sophisticated technological system that, in seconds, simultaneously contacts and quotes from the databases of dozens of the largest, best-capitalized, and most respected insurers legally operating in the state. By forcing fierce, real-time competition among these multiple companies for the right to win your business, Univista clinically and transparently identifies the exact policy that mathematically matches your current risk level. This model ensures you obtain the lowest possible and justified rates immediately on the same day of quoting, stopping at the root the financial mistake of underwriting inflated premiums that end up becoming, years later, obsolete and restrictive statutory refunds. You keep your capital; the insurer assumes the risk at the right price.

Beyond the refund headlines, have auto insurance prices and base rates in Florida actually, verifiably, gone down for the 2025-2026 period?

Yes, there is solid statistical evidence, actuarially validated by the state, supporting a real trend reversal. According to extensive public reports and appearances by the Office of Insurance Regulation (OIR) Commissioner, Mike Yaworsky, the five largest and most dominant corporate auto insurance groups in the Florida market (who dictate the pulse of pricing) averaged an official request for a base rate reduction of -6.5% for calendar year 2025. In documented individual cases within the state, some insurers even submitted rate reduction requests to the regulator of up to an astonishing -11.5%. This concerted and regulated downward action marks, with strong certainty, the closing and settlement of long, painful, and consecutive years of aggressive double-digit increases.

Long-Term Actuarial Market Projections (2026-2030): The Era of Stability, AI Infiltration, and Fierce Competition

As the state of Florida macroeconomically absorbs the immense liquidity shock of the projected $1 billion refund and methodically adjusts its structural rates downward to the new post-litigation normal, the entire insurance market ecosystem (both property and casualty) is crossing a critical inflection point toward maturity, predictability, and stabilization.

Industry analysts foresee tectonic shifts in the way insurance will be structured and consumed in the final stretch toward 2030.

Rate Stability and Global Reinsurance Confidence

Chaotic and almost untamable volatility is, for the most part, a thing of the past. Governor DeSantis, backed by top OIR technical authorities, has repeatedly expressed immense institutional confidence and has received, crucially for the state’s economy, the explicit backing and blessing of the global reinsurance market (the capital from London, Bermuda, and Zurich that backs local insurers). The international financial world now perceives and categorizes Florida as a legally safe, rationalized, and therefore profitable territory to operate in. This shift in perception is attracting massive amounts of new private venture capital and fostering the entry and competitive return of multiple insurers to the state.

From the consumer pricing perspective, actuarial models firmly project that drastic, spasmodic, and painful annual rate adjustments (such as the traumatic generalized spikes of 15% to 31% annually that Floridian citizens experienced and suffered at the beginning of the decade) will gradually give way to an operating environment of “boring stability” but economically welcome. Experts project that annual premium fluctuations will flatten, stabilizing predictably in ranges of 2% to 4%. These small, gradual increases will not be driven by legal crises, but simply to remain in strict accordance with the inescapable march of underlying macroeconomic inflation that intrinsically affects the costs of vehicle repair supply chains, replacement parts, and the provision of post-accident medical care.

The Quantum Leap of Artificial Intelligence (AI) in Underwriting

The next quantum and truly transformative leap in insurer profitability and relentless efficiency in real-time pricing for the consumer will be inexorably led by the deep and systemic integration of Artificial Intelligence (AI) and Machine Learning.

As the state of Florida carefully and pioneeringly navigates the implementation of new, robust, and necessary AI ethical regulations specific to the insurance sector (such as the highly technical and legislative debates surrounding the HB 527 bill), it is undeniable that these cutting-edge algorithmic tools will act as potent catalysts. AI will radically accelerate the volumetric evaluation and processing of claims, almost infallibly detect complex anomalies indicative of systemic fraud or organized accident syndicates that previously went unnoticed by human inspectors, and most impactfully for rates, issue telematics models and individual risk profiles that are much more granular and of unprecedented hyper-personalization.

However, the unanimous consensus of industry sages and regulatory bodies (as well as the unwavering pillar of Univista Insurance’s philosophy and prolonged success) conclusively maintains and deeply warns that, while AI technology is a highly potent logistical and numerical analysis accelerator, “the definitive final decisions and judgments regarding coverage, payments, and insurance care must inescapably remain a human prerogative.” Risk, loss, and recovery are, at their fundamental core, human experiences.

Univista Insurance’s technological deployment perfectly embodies and executes the masterful synthesis of this modern hybrid concept. While its digital infrastructure and proprietary AI facilitate the overwhelming speed of multidimensional quoting and its virtual assistant (“Mayra”) provides entry-level consultation capacity and uninterrupted administrative assistance 24 hours a day, 7 days a week, critical human judgment is never displaced. It is the thousands of physical, licensed Univista agents—professionals fully and empathetically immersed daily in the cultural fabric, economic dynamism, language, and unique social geography of South Florida—who ultimately masterfully guide the final determinations of coverage architecture and who provide the invaluable and irreplaceable human, moral, and logistical support during the confusing moments following major catastrophic events, hurricanes, or severe financial losses due to structural claims.

The Triumph of Rationality and Proactivity over Economic Reactivity in Insurance

In a retrospective analysis of the tumultuous period spanning from the pricing crisis to the current rectification, the aggressive and controversial judicial reforms firmly led by the Florida government administration at the beginning of the decade have undeniably and resoundingly achieved the primary macroeconomic and systemic objective for which they were arduously designed, lobbied, and finally enacted into law: forcefully suppressing the crippling costs derived from abusive litigation that ate away at the industry’s foundations and drastically increasing, as a reflex effect, the operational solvency, technical viability, and massive financial profitability of the state’s auto insurance market.

The spectacular collateral economic consequence of this new market health—the colossal legally anticipated and inexorable return of an estimated $1 billion in pure, auditable excess corporate profits directly into the pockets of long-suffering taxpayers, under the severe protection and strict application of Regulatory Statute 627.066—historically and undoubtedly serves as a powerful, functional, and indispensable legislative checkpoint. This forced refund demonstrates that the state’s intricate legal machinery does function as the ultimate retaining wall to ensure that this sudden, immense, and new corporate prosperity derived from the reforms is shared, enforced by the iron rule of law, with the average consumer of the “Sunshine State.”

However, beneath the superficial gloss of journalistic optimism invariably radiated by these government announcements and refund checks, lies exposed a stark, fundamental, and undeniable master class in strict personal economics and household risk management. Analyzed coldly and numerically, a massive corporate refund of these epic proportions is not a bonus; it is a flashing red warning beacon, as it inevitably exposes and quantifies the corrosive impact of three long years of structural overpricing suffered by the population.

The irrefutable analytical conclusion is that being trapped by inertia, marketing, or ignorance in the opaque and closed ecosystem of a single or captive direct insurer and carrier almost invariably translates in the long run into blindly subsidizing, with one’s own interest-free capital, corporate risk aversion, fattening their treasury fund, and then passively sitting and waiting lightyears in the hope that at some future point the state’s arduous punitive and regulatory mechanisms will intervene to de facto force the return of your own hijacked money.

In the unforgiving but opportunity-rich competitive market of 2026, the awakened and informed Florida citizen urgently demands and requires immensely superior tactical and financial armor. The advanced operational methodology of true independent insurance agencies, brought to its highest and purest expression by the unmatched and unbeatable commercial infrastructure, logistical scale, prestige, and innovation of Univista Insurance, categorically represents the inevitable and necessary Darwinian evolution in the intelligent and strategic acquisition of any type of asset risk coverage.

By unrestrictedly mobilizing powerful, next-generation simultaneous comparative systems and engines in its favor in the free market; by offering invaluable, ethical, and dedicated expert bilingual local fiduciary advice—deeply backed by an irrefutable history of more than a decade of relentless expansion and proven, award-winning success—; and through the ironclad, unquestionable, and auditable commitment to accurately, mathematically, and fully transparently quoting and securing the fair price at all times, Univista Insurance subverts, dismantles, and fundamentally transforms the classic and harmful asymmetrical power dynamic in the consumer’s interaction with the insurance product.

This new architecture allows transitioning from the obsolete and detrimental model of “blindly overpaying, crossing fingers, and passively waiting for the late corporate refund handout,” to rise vigorously toward a proactive, dignified, and modern paradigm characterized by relentless real-time cost optimization and immediate results, obtaining legally airtight and unquestionable coverage in its entire extent for family peace of mind, and above all, the ironclad, non-negotiable retention of your own hard-earned economic capital from minute one, the first business day, and continuously throughout the total duration of the policy. Faced with the ever-uncertain fleeting promises of receiving possible inflation-depleted corporate checks lost in the mail maze in the future and subject to cumbersome eligibility deadlines, the immovable contractual certainty of holding a fair, optimal, and guaranteed price in hand in the strict present continues, today and always, to constitute the greatest, most unbreakable, and astute financial policy and protective shield any rational mind can acquire and forge.

Vehicle

Vehicle